We are living in the 21st century where things change like seasons! The financial sector has evolved rapidly over a decade (thanks to technology) software,…

Fintech as a term described in Wikipedia is as follows, “FinTech is the new applications, processes, products, or business models in the financial services industry,…

People in India seem to be drawn towards cryptocurrencies, even though the government tried to curb the growth of the digital currency market. The year…

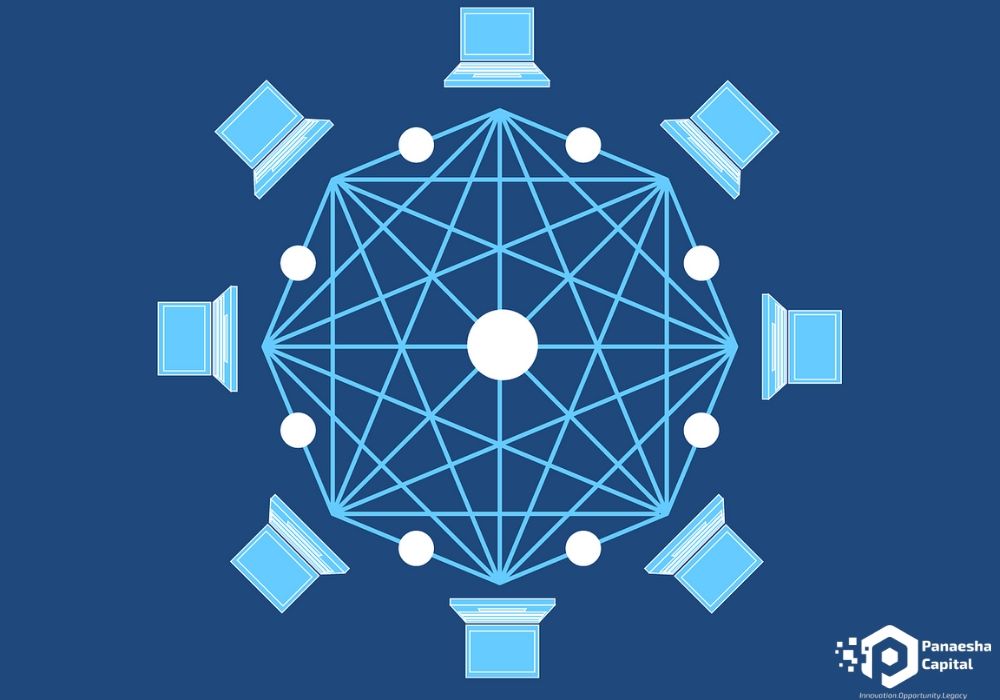

“Technology is neither good nor bad; nor is it neutral.” – Melvin Kranzberg Technology, specifically blockchain technology has changed a lot about how we operate.…

“Technology is anything that wasn’t around when you were born” – Alan Kay Financial Technology or Fintech is an industry that evolved for the spontaneity…

Fintech is being used across all financial services functions. Even the replacement of paperwork to digital processes in an example of fintech. Below are a…

In an industry brimming with start-ups, why will Panaesha Capital stand out? Panaesha Capital PVT. LTD. has a goal that any noteworthy company, start-up or…