Blockchain is a resourceful and farsighted invention of the human. The technology is viewed to bring meaningful and significant changes in the system of finance.…

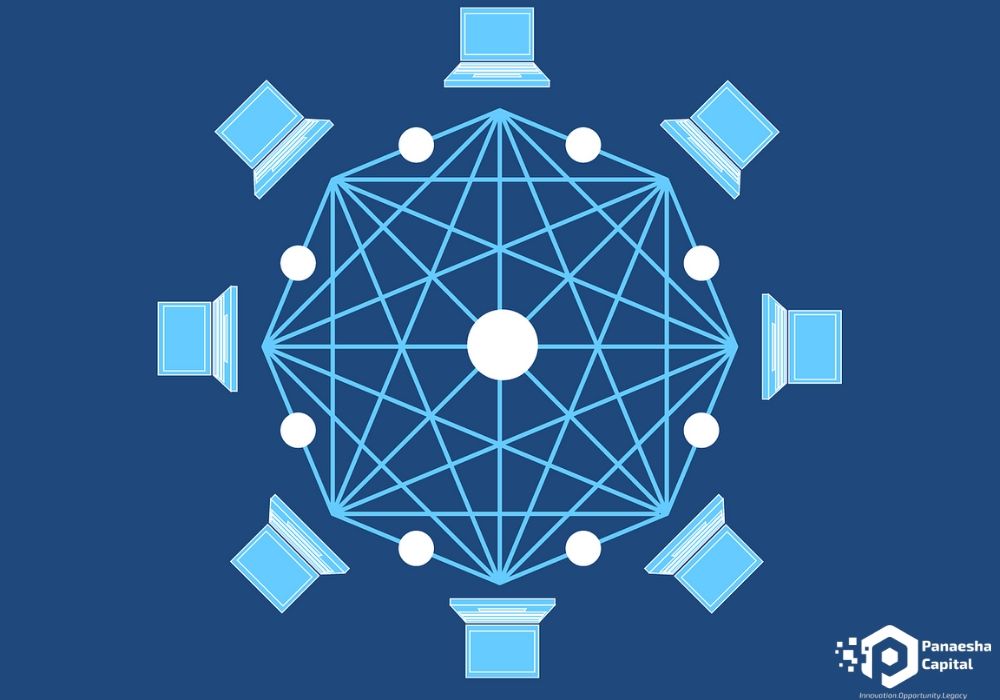

Blockchain Technology has increasingly gained importance over the past years. From disrupting the working of industries to changing the way we live our day-to-day life,…

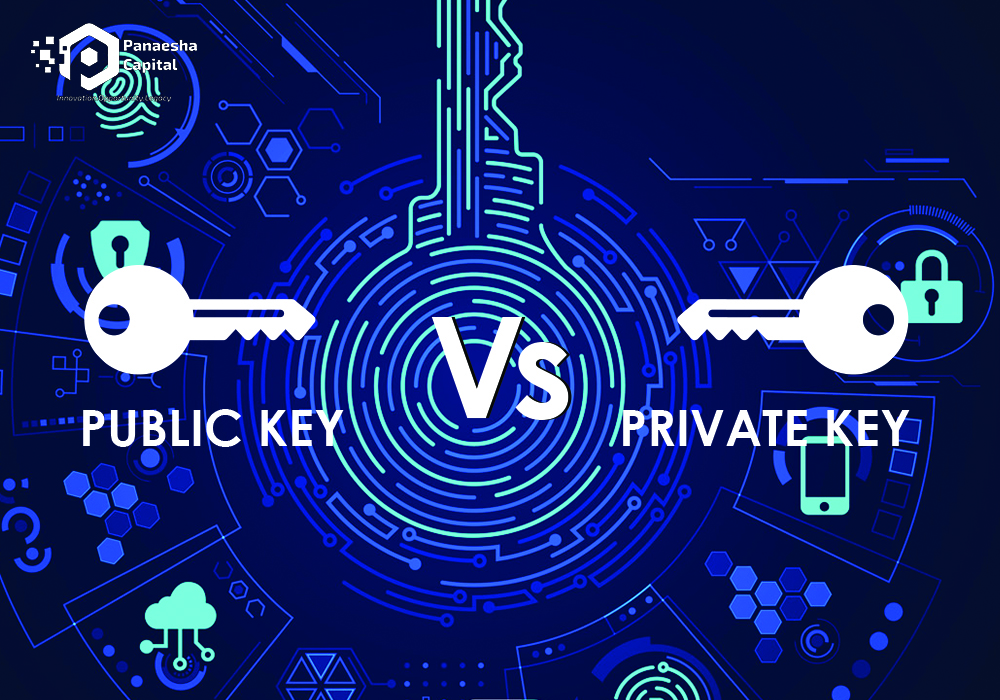

The Public key and Private key are the cryptographic keys that are used to lock and unlock cryptographic functions including authentication, authorization, and encryption. Cryptographic…

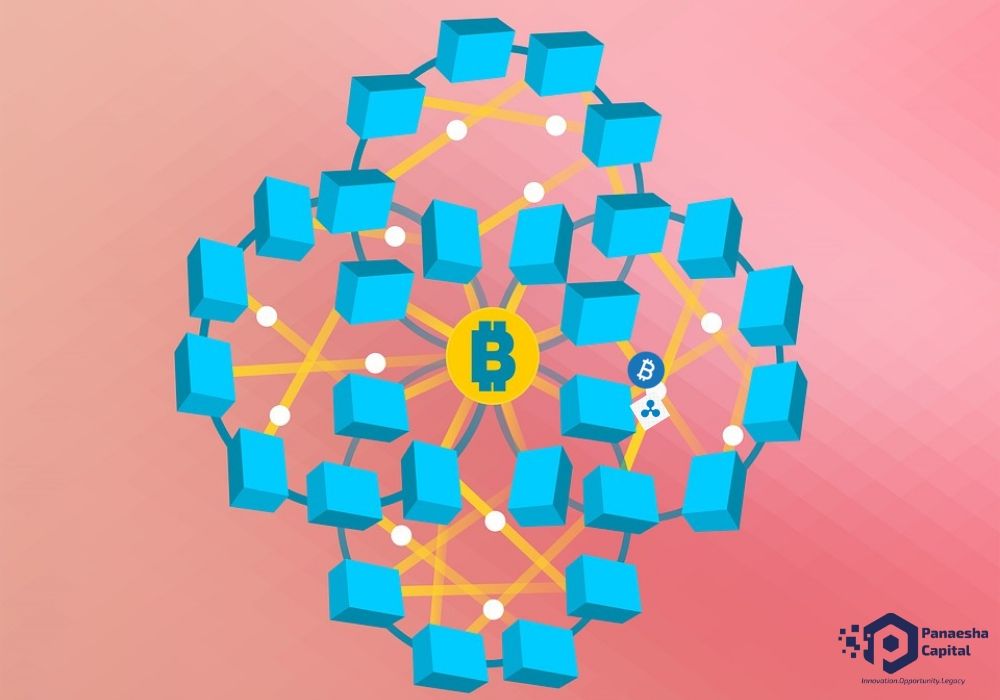

The blockchain technology has influenced and helped many sectors since its inception in 2008. This technology is extremely advanced and has no competition as of…

Master Data is one of the most important and critical property that a business can possess. With the upcoming fourth industrial revolution, the significance of…

Fintech as a term described in Wikipedia is as follows, “FinTech is the new applications, processes, products, or business models in the financial services industry,…

We have got used to hearing about new and innovative projects with blockchain as the underlying technology. Whether it is an online marketplace or green…